Stocks were relatively flat last week in the face of weak economic data. Services, manufacturing, and job openings all were weak, but the monthly jobs data (more below) was a bright spot. Still, in the face of slowing economic reports, we were impressed stocks were able to hold onto some gains.

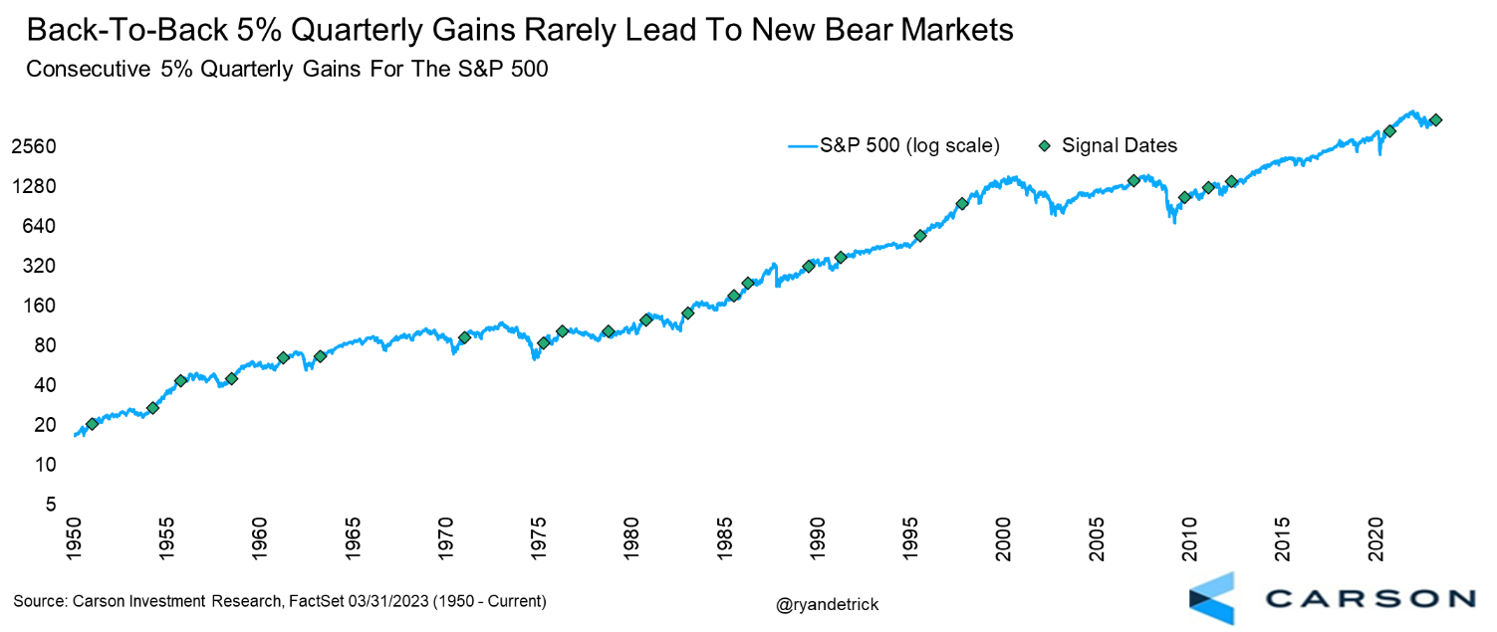

- Stocks soared two quarters in a row, which is consistent with stronger future returns.

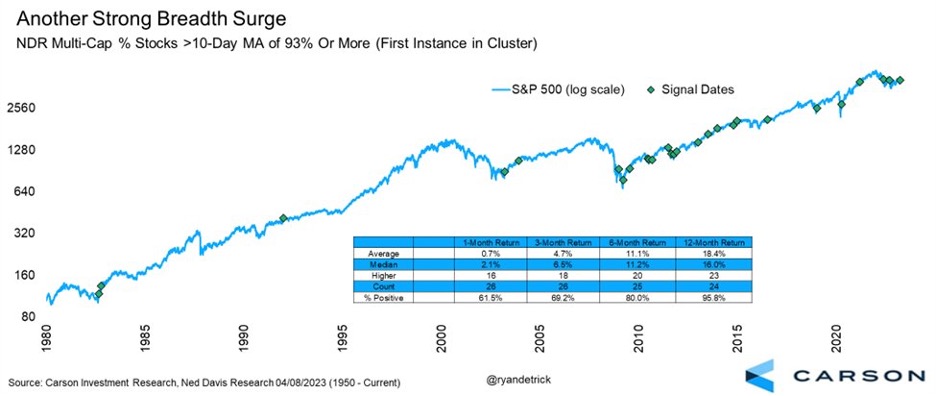

- Market breadth isn’t as negative as many believe, which is another plus for stocks.

- The banking crisis, a recent softening in job openings, and higher unemployment claims have raised concerns of a labor market slowdown.

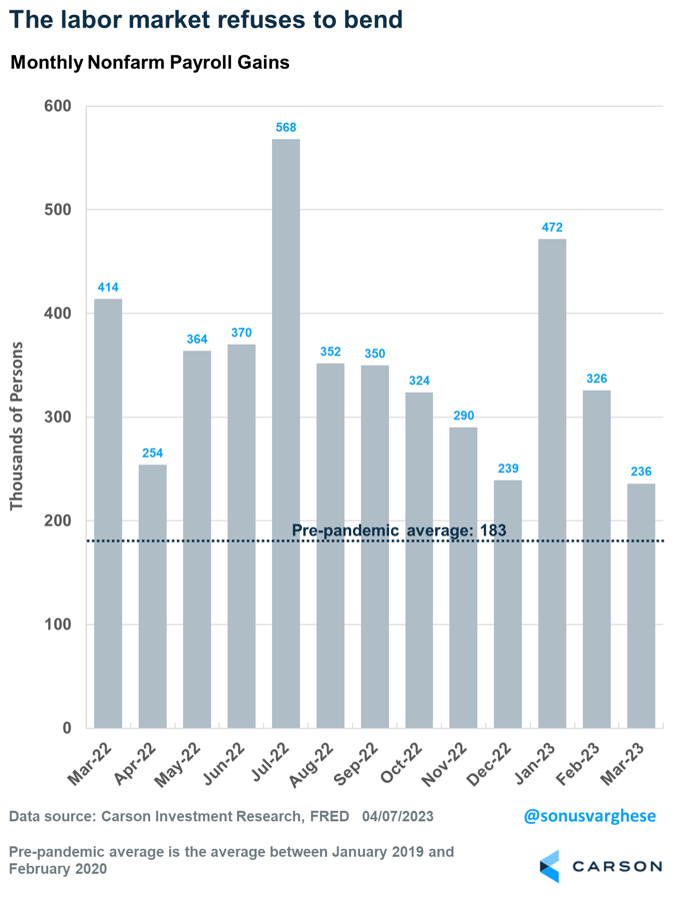

- The March employment report was strong, with 236,000 jobs created.

- The unemployment rate is 3.5%, near 50-plus year lows.

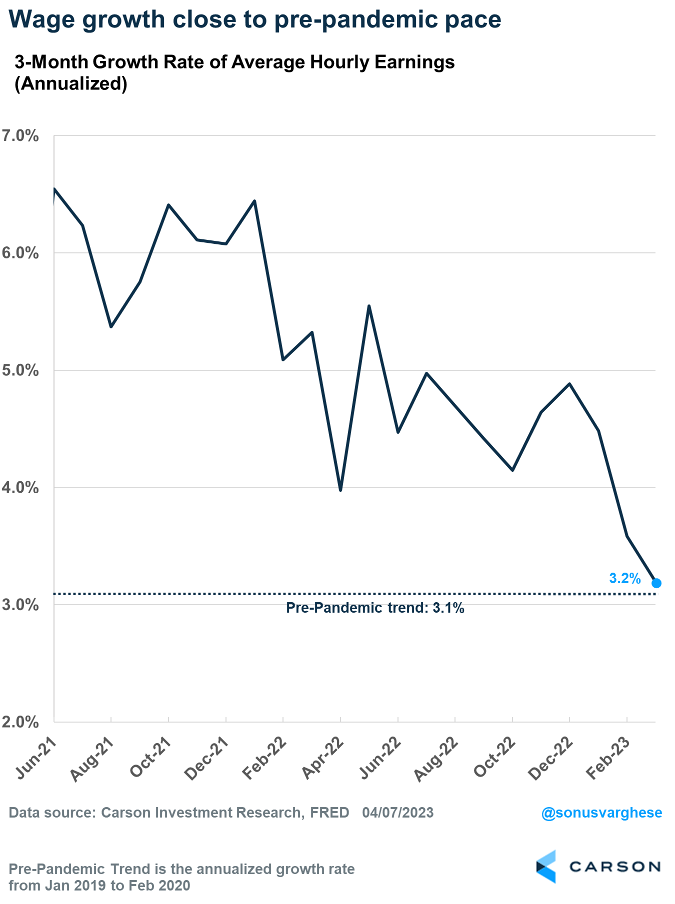

- Wage growth is simultaneously decelerating, which should be enough reason for the Fed to ease up on further rate hikes.

We continue to be cautiously bullish overall, and one reason is that after gaining 7.1% in the fourth quarter, the S&P 500 added another solid 7.0% (price only, no dividends) last quarter. Many market watchers have been calling this a bear market rally, but history shows that consecutive 5% quarters rarely happen in the middle of bear markets. More often than not, they occur at the start of new bull markets. As the chart below shows, this rare signal suggests the potential for more strength, not the start of a new bear market. In fact, two quarters later stocks have been higher 21 out of the past 23 times after this bullish signal.

Some are raising concerns that only a few stocks are pulling the market higher, saying this indicates poor market breadth, which could signal cracks in the armor and a potential fall. However, this is not true as many stocks have been advancing.

In fact, more than 93% of all stocks tracked by Ned Davis Research recently climbed above their 10-day moving averages. This rare sign of strength has led to higher prices for the S&P 500 23 out of 24 times one year later and an average return of 18.4% on average.

The Labor Market Refuses to Bend

Prior to the release of the March payroll report, there were several indications that the labor market was headed for a slowdown. January and February payrolls were well above expectations, leading to concerns that the strength was due to seasonal factors that would reverse. Then Silicon Valley Bank crashed in early March, raising fears the economy would buckle if a widespread banking crisis followed.

Then, last week, the Bureau of Labor Statistics (BLS) released data that showed job openings fell below 10 million in February, the lowest level since May 2021. Despite being well above the near-7 million openings pre-pandemic, it indicated labor demand was softening. (We would like to note this is precisely what Federal Reserve officials were hoping to see.) In addition, the BLS revised all unemployment benefit claims data going back to 2018. This is typically a leading indicator for the labor market, and the news wasn’t good. Claims for unemployment benefits have been steadily rising since October — not by enough for a recession to be imminent but enough to be concerned.

So, the March payroll release had a lot riding on it as investors and economists wondered if the data would corroborate these concerns.

Short answer: No.

Instead, we got yet another solid payroll report, with 236,000 jobs created in March. While below the 346,000 average of the prior three months, this is very strong. The economy was creating about 180,000 jobs a month prior to the pandemic and needs 100,000 or so to keep up with population growth. It is currently more than doubling that amount.

Moreover, the unemployment rate fell to 3.5% and is just a tick above its lowest rate in 50-plus years. And that happened despite almost 500,000 more people entering the labor force. This belies concerns that the labor market is “supply-constrained” and the Fed must somehow force demand lower to match supply. Instead, we have a strong job market in which employers want to continue hiring, and that is making workers and potential workers more confident to start looking for jobs.

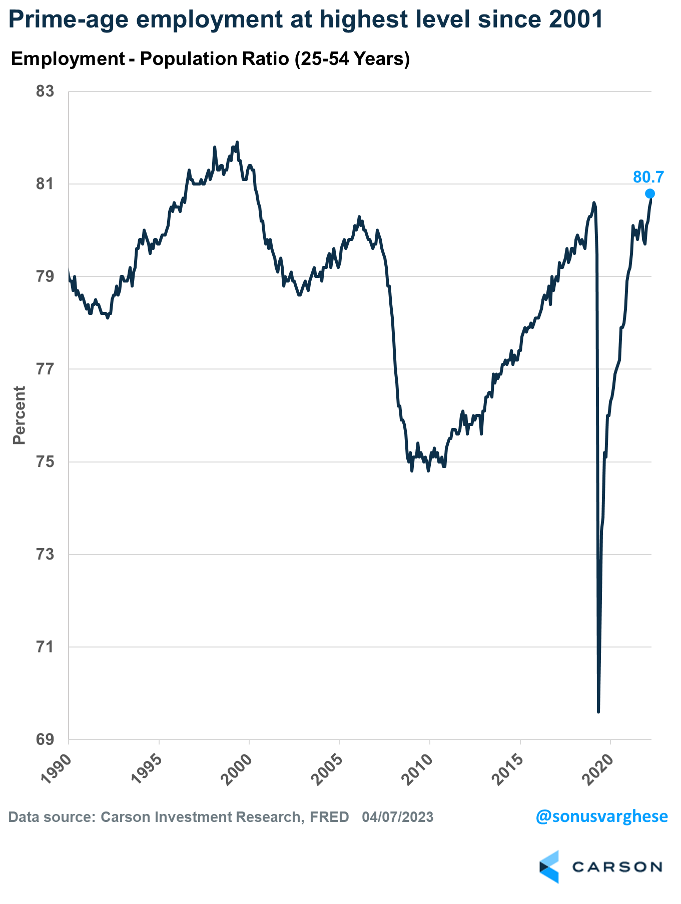

Perhaps the best indicator is the employment-population ratio for prime-age workers (25-55 years). In a sense the opposite of unemployment, this indicator measures employment for people in their prime working years as a percentage of the civilian working-age population. It also avoids issues related to an aging population and people who the BLS considers not part of the labor force for various reasons, such as lack of childcare. The measure rose to 80.7%, which is the highest level since 2001 and a sign that this is a strong labor market.

Good News for the Fed

What’s most positive is the unemployment rate is near historic lows even as wage growth is decelerating. Over the past three months, average hourly earnings for private sector workers rose at an annualized pace of 3.2%, which is barely above pre-pandemic levels.

Fed officials have tied inflation, especially services excluding housing, to wage growth. Decelerating wage growth should give them enough reason to pause on further interest rate hikes, as inflation is likely to continue trending lower over the rest of 2023. Given their aggressive pace of rate hikes over the past year, and their most recent hike, which they implemented despite being within two weeks of a banking crisis, we believe there is enough justification for a pause.

We also believe the employment data implies the economy is still positioned to avoid a recession this year. That means it’s highly unlikely the Fed will cut rates, as Fed officials themselves continue to stress. However, markets are expecting the Fed to cut rates by at least 0.75% by the end of this year. So, expect some volatility in bond markets as investors’ views converge with the Fed’s.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01725733