Equity markets struggled in September as interest rates, inflation concerns, and developments in China all weighed on stock market averages. The S&P 500 surrendered 4.7% as large-cap growth companies led the market lower. Large-cap growth has been the top performing style box since the beginning of the second quarter.

Key Points for the Week

- Equity markets wrapped up the worst month of the year. Interest rates, inflation concerns, and developments in China all weighed on equities in September.

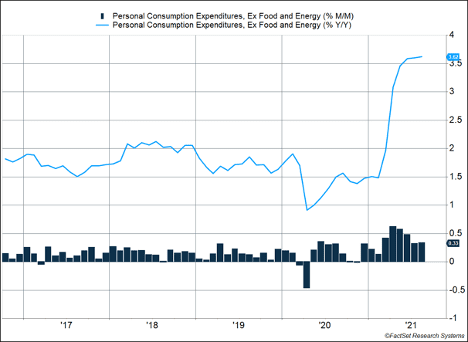

- August core PCE rose 0.3%, but the rate of increases continues to moderate. Energy and food are still driving headline inflation figures.

- Legislation was signed Thursday evening to avoid a partial federal government shutdown, keeping the government funded through Dec. 3.

Inflation continues to show signs of moderating in the U.S. while remaining above pre-pandemic levels. As shown in Figure 1, yearly inflation inched higher. Investors who focus on the annual data may miss the monthly data in the bars at the bottom of the graph. The last two months have increased 0.3%, which is faster than before the pandemic but slower than earlier this year.

As expected, lawmakers reached a compromise to avoid a partial government shutdown. We expect to see continued brinkmanship on key issues. Democrats also continue to work on cobbling together majorities for infrastructure and spending bills.

The S&P 500 sagged 2.2% in a volatile week. The MSCI ACWI shed 2.4%. The S&P’s decline was the largest weekly dip since late February. Concerns about increasing long-term interest rates contributed to the slide. The Bloomberg U.S. Aggregate Bond Index added to last week’s losses, falling 0.1%. The September employment report leads a list of economic releases this week.

Figure 1

Risk On

Traders sometimes use the phrases “risk on” and “risk off” to describe trades or positioning designed to profit from market rallies or protect from market declines. But the reality is risks are always present and predicting short-term market moves is extremely difficult.

While risk is constant in the markets, portfolios face greater risks at certain times. Being prepared can reduce the odds of a rash move to lower risk when the market declines. Identifying specific risks also helps to keep them top of mind and balances the temptation to chase higher returns.

Each quarter we analyze the five key risks in the market and provide a summary of why those risks were added or retained on our list. Today’s update shares our current list of key risks.

- Virus variants: A restaurant with empty tables used to mean no wait time. Today, half the tables can be empty, and you can still wait an extra 20 minutes. The Delta variant has slowed the willingness of workers to return to the workforce. The variant is highly transmissible, and some studies have shown waning effectiveness of vaccines against it. Our top risk is the next variant could prove to be more challenging.

- China: Last week’s incursion by the Chinese air force into Taiwan’s defense zone and recent concerns about property developers in China are just two ways the Middle Kingdom is contributing to market risk. China is the world’s second largest economy and the largest market for several key industries. It also plays a crucial role in the global supply chain. Any challenges coming from China are likely to affect the rest of the world.

- Policy mistake: The risk of a policy mistake remains in our top five but has likely lessened. Third quarter economic data showed inflation trends are moderating while growth data remain relatively strong. The risk of the Fed being forced to respond to heightened inflation and surprise the markets seems lower. Economic data point to the recovery being strong enough to need less help from the Fed.

- Supply chains: Shortages from microchips to chicken wings continue to pressure the recovery. Our view is the innovative power of capitalism will overcome these shortages eventually. But any of the previous three risks could trigger additional shortages, whether from fewer new workers, a trade war, or a policy decision that hits a vulnerable industry. The U.K.’s difficulty in finding truck drivers shows how COVID and Brexit interacted to create a much greater challenge than expected.

- Investor behavior: The third quarter marked the sixth straight quarterly increase in the S&P 500. Stock investors have done well, and the market has rewarded those who pushed the risk envelope. In the third quarter, the S&P 500 only increased 0.6%. Those returns were better than bonds and cash but may not be enough reward for the additional risk borne by stock investors.

Our view remains many investors have left themselves emotionally vulnerable to a market pullback that may exacerbate a moderate decline. At the same time, history has taught us most market risks are either managed, mitigated, or innovated away and that an optimistic outlook remains the most prudent. Please work with your advisor if you are concerned your portfolio reflects too strong a tilt in either the “risk on” or “risk off” direction.

—

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://www.worldometers.info/coronavirus/country/us

https://www.gobankingrates.com/money/economy/when-will-chip-shortage-end-experts-weigh-in/

https://www.gobankingrates.com/saving-money/food/national-chicken-wing-shortage-prices-are-rising/

https://www.bbc.com/news/57810729

Compliance Case #01148244