Central banks are playing the leading role in today’s markets. Last week, the European Central Bank raised interest rates 0.5%, pulling the deposit facility rate to 0%. It is the first interest rate increase in 11 years and the first time the rate hasn’t been negative in eight years. Japan’s central bank took a different approach, leaving rates stable. The Japanese Consumer Price Index has only risen 2.3% in the last year. That is much higher than normal but close to the target of 2%.

Key Points for the Week

- The European Central Bank joined the inflation fight, raising rates 0.5%. Japan left rates unchanged.

- The United Kingdom continues to lead all G7 countries with a 9.4% inflation rate.

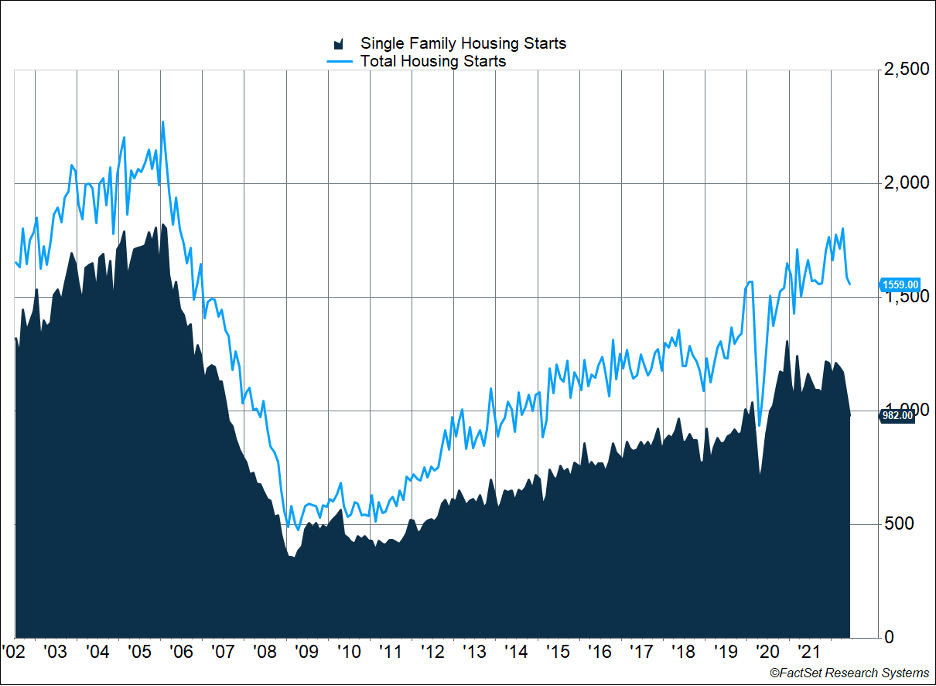

- Housing starts fell 2% last month as higher interest rates pushed demand lower.

The U.K. is on the other end of the inflation spectrum. Inflation in Britain jumped 0.8% last month and is now 9.4% higher than one year ago. The Bank of England indicated a 0.50% hike is possible at the next meeting given that inflation has remained elevated despite a steady stream of 0.25% rate increases.

The domestic housing market is starting to respond to higher interest rates in the U.S. Housing starts fell 2%, the second straight monthly decline (Figure 1). The Federal Reserve is likely to reduce demand further by increasing interest rates 0.75% at its meeting this week.

Markets seem to have priced many of these events in already. The S&P 500 gained 2.6% last week. The global MSCI ACWI rebounded 3.2%. The Bloomberg Aggregate Bond Index rallied 0.7% as long-term rates declined despite the widely expected additional rate increases.

Figure 1

Nearly a Full Court Press

In basketball, a full court press is when the defense pressures the offense the entire length of the floor. Every player needs to exert significant effort for a press to be successful. If only three of the players are trying to press and the rest are not, the press will be broken fairly easily. Global central banks are engaging in their own version of the full court press against inflation as more central banks are joining the effort to reduce excess global demand. Until last week three major players hadn’t raised rates: the European Union, China, and Japan. We will examine each country as we look toward the Federal Reserve interest rate decision this week.

The European Central Bank surprised markets last week by raising interest rates 0.50% to 0%. The reason this is so surprising is it is the first time in 11 years that the ECB increased interest rates. In fact, this is the first time in eight years that the deposit rate in Europe is positive. The market expected the increase to be 0.25%, but June’s outsized inflation report at 8.6% caused the ECB to raise rates more aggressively.

Interestingly, the ECB didn’t provide any forward guidance on moves it may make later this year. It has signaled it will be data-dependent, meaning it will wait to see what the July inflation number looks like. One reason the ECB may be hesitant to raise rates too quickly is Europe’s inflation is being driven by supply issues, especially on energy due to the conflict in Russia. The European economy has weakened as the sanctions on Russia have slowed growth. Exacerbating the problem is weakness in the euro. The euro is as weak as it’s been in the past 20 years, which is making energy imports priced in U.S. dollars even more expensive. A 0.50% increase showed markets the ECB was serious, while the lack of future guidance reflects the weak European economy.

Japan’s central bank has been the lone holdout of major developed economies. The Bank of Japan announced last week that it would keep interest rates unchanged, with its short-term rates remaining at -0.1. This comes despite the weakest level for the yen versus the U.S. dollar since 1998. The fear from BOJ governors is that any increase in rates, even to stop the fall of the yen, would be too damaging to Japan’s economic recovery. The difference is Japan is experiencing much more muted inflation than the U.S. and Europe. The expectation in Japan is that core inflation will increase by only 2.3% over the next year.

China’s monetary policy has moved in the opposite direction from the rest of the world. The Chinese have actually cut rates and taken other steps to invigorate the economy. At first glance this doesn’t make much sense, as China is a big importer of energy. China’s situation is different because it will buy oil from Russia, likely at a lower price than what the rest of the world pays. It also continues to lock down cities and engage in strong forms of social distancing. By restricting activity, the Chinese are effectively pushing down demand for all sorts of goods and services, and those policies are likely doing more to slow their economy than a 0.50% rate hike.

We expect central banks to ratchet up the pressure more next week. The Fed is expected to raise rates 0.75% when its meeting concludes on Wednesday, matching June’s increase. Any other outcome would be surprising. Fed Chair Jerome Powell’s press conference after the meeting will be watched closely for future guidance. If rates move up 0.75%, the target rate will be 2.25-2.5%, which is above what the economy could sustain before COVID.

Our expectation is the broad number of nations tightening policy will start to reduce the effects of excess demand on inflation and remove some of the pressure from supply-constrained markets at the same time. The Fed moving rates past what many believe is neutral means short-term rates will be working to slow the economy. The ECB moving rates to 0% means the strange incentives encouraged by negative rates will disappear. Every rate hike helps to slow the economy, but the ECB hike last week and the expected Fed move this week are key events in the fight against inflation.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

BLOOMBERG U.S. AGGREGATE BOND

The Bloomberg US Agg Total Return Value Unhedged, also known as “Bloomberg U.S. Aggregate Bond Index” formerly known as the “Barclays Capital U.S. Aggregate Bond Index”, and prior to that, “Lehman Aggregate Bond Index,” is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency).

Wall Street Journal. Megumi Fujikawa. 7/21/2022. https://www.wsj.com/articles/bank-of-japan-sees-inflation-hitting-2-3-this-fiscal-year-11658374450

Wall Street Journal. The Editorial Board. 7/21/2022. https://www.wsj.com/articles/the-ecb-raises-while-mario-draghi-falls-christine-lagarde-european-central-bank-interest-rates-italy-11658426371

Financial Times. Chris Giles. 7/20/2022. https://www.ft.com/content/e777a2d1-bc5c-4e01-8605-2be0682aad5e

US Census Bureau. 7/19/2022. https://www.census.gov/construction/nrc/pdf/newresconst.pdf

VOA. 7/06/2022. https://www.voanews.com/a/fresh-covid-19-outbreaks-put-millions-under-lockdown-in-china/6648113.html

CME Group. 07/24/2022. https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

Compliance Case #01439315