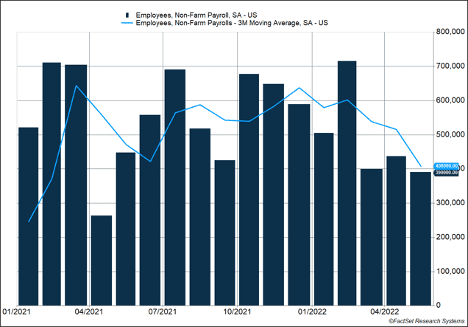

The S&P 500 dropped 1.2% last week as a strong employment report was a little “too good” and raised concerns of more interest rate hikes in the future. The U.S. economy added 390,000 jobs in May, based on the establishment survey. Job growth is slowing, but it remains well above the level required to provide jobs for new workers entering the labor force for the first time.

Key Points for the Week

- The U.S. economy produced 390,000 new jobs last month and the unemployment rate remained at 3.6%.

- Average hourly earnings increased 0.3% last month, reflecting moderate wage pressures in the economy.

- Stocks and bonds declined as markets focused more on the likelihood of additional rate hikes than the generally positive jobs report.

The corresponding household survey also contained good news. Unemployment dropped to 3.6% and the percentage of people employed rose 0.1% to 60.1%. Average hourly earnings remain contained, rising 0.3% for the second consecutive month.

The JOLTS survey, which measures job openings, indicated available positions dipped slightly but stayed above 11 million. The large number of unfilled positions is another indication the labor market is “too good.” The Federal Reserve would view additional declines in the number of openings as a positive step that reduces the pressure to raise rates. The trend towards lower openings may have already started as some technology companies have announced plans to slow hiring or lay off staff.

Global stocks also declined last week. The MSCI ACWI sagged 0.5%. The Bloomberg U.S. Aggregate Bond Index gave back 0.9% of its recent gains. The Consumer Price Index will be the big data release of the week and provide further indication of how quickly consumer prices are increasing.

Figure 1

A Little Too Good

Last week the market reacted negatively to a very positive employment report. As mentioned above, the S&P 500 dipped 1.2%, giving back a portion of the previous week’s 6.6% rally. Markets were higher last week, through Thursday, but declined enough on Friday to turn the gains into a loss. The market decline was precipitated by concerns the Fed would raise interest rates more than desired in response to the strong jobs data.

The employment situation in the U.S. definitely favors the employee more than in recent decades. There are more than 11 million job openings in the U.S., and for inflation to get under better control, this number needs to move lower. The lack of workers in a period of heightened demand has contributed to higher inflation.

But more people are joining the labor force, which means the supply of goods reaching stores and services that are in short supply can now be provided. Some people taking new positions are entering the workforce for the first time, but others are returning after being away. The employment-population ratio increased from 60.0% to 60.1%. Although a more rapid increase would have been better, the data show people are steadily returning to the labor force. Prime-age employment (25-54) ticked up to 80%, which is in line with peaks seen in 2006 and 2020.

Average hourly earnings increased 0.3%, which roughly matched the previous month. In the last 12 months, hourly earnings have increased 5.2%, a monthly rise of more than 0.4%. Higher wages can lead to inflation becoming more entrenched than it already is, so a 0.3% rise suggests wage inflation is close to the long-term target.

Amid many strong data points, there are signs the labor market is starting to slow to more manageable levels. The JOLTS survey for April indicated openings fell 455,000 to 11.4 million. After frequent records, the job opening trend is moving in the right direction. Retail trade openings experienced the biggest declines, and retail employment also fell in the May report. Large retailers mentioned in their earnings reports that they were overstaffed, so a decrease in that one sector isn’t surprising.

Another positive trend is more companies are announcing a reduction in job openings and even some layoffs. Given how low unemployment is, having some companies lay off workers likely helps reduce inflationary pressures even as it is difficult for the workers and their families.

Our view is the data last week should have been viewed more positively. Job growth is moderating toward a level that is neither too hot nor too cold. May had the lowest number of new jobs created in the last 13 months yet was strong enough to indicate the economy is performing well.

The market rightly raised its expectations for interest-rate hikes by elevating the probability of three more 0.5% increases in the next three meetings. The data show the economy is stronger than anticipated. That strength also means a recession is less likely and the risk of a recession is pushed into the future. The decline in unfilled positions and the increase in the number of people working are positive trends that indicate progress toward a better balance between the demand and supply of labor.

Sometimes the market gets too focused on the Fed keeping rates low or looking at weaknesses in the report. This jobs report indicates the economy remains healthy and key data points are moving in the right direction.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

https://www.bls.gov/news.release/pdf/empsit.pdf

https://asia.nikkei.com/Business/Startups/Tech-startup-layoffs-top-20-000-amid-big-funding-chill

https://www.bls.gov/news.release/jolts.nr0.htm

Compliance Case #01393143