After a large reversal Thursday, stocks bounced back Friday, bolstered by the continued impressive performance of the economy (further details below). This has already been a historic year — the stock market experienced one of its best starts in 2023. The S&P 500 is up close to 20% for the first seven months, and the Nasdaq is up even more.

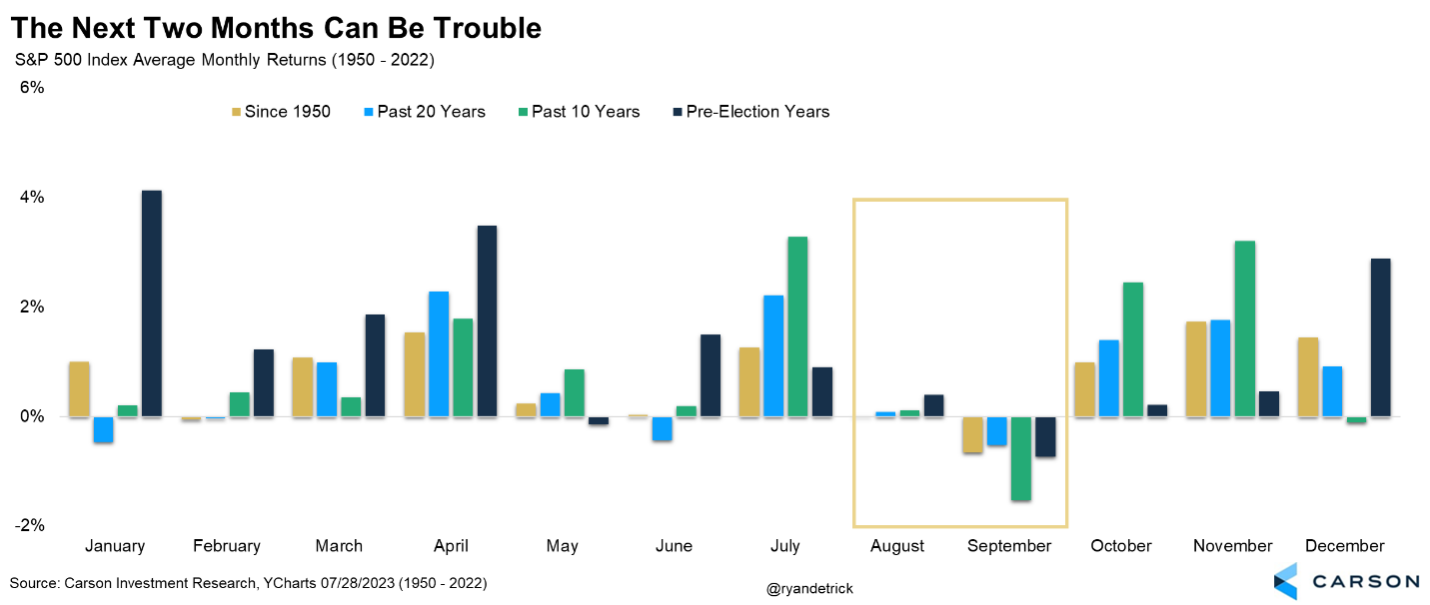

- Stocks have had a great run, but August and September are typically weak.

- If seasonal weakness occurs, it may be modest. Higher prices before year-end remain likely.

- The Federal Reserve hiked rates for the 11th time in 17 months, taking them to the 5.25-5.50% range.

- The Fed is waiting for core inflation to pull back, and there are indications this is occurring, potentially making the latest rate hike the final one of this cycle.

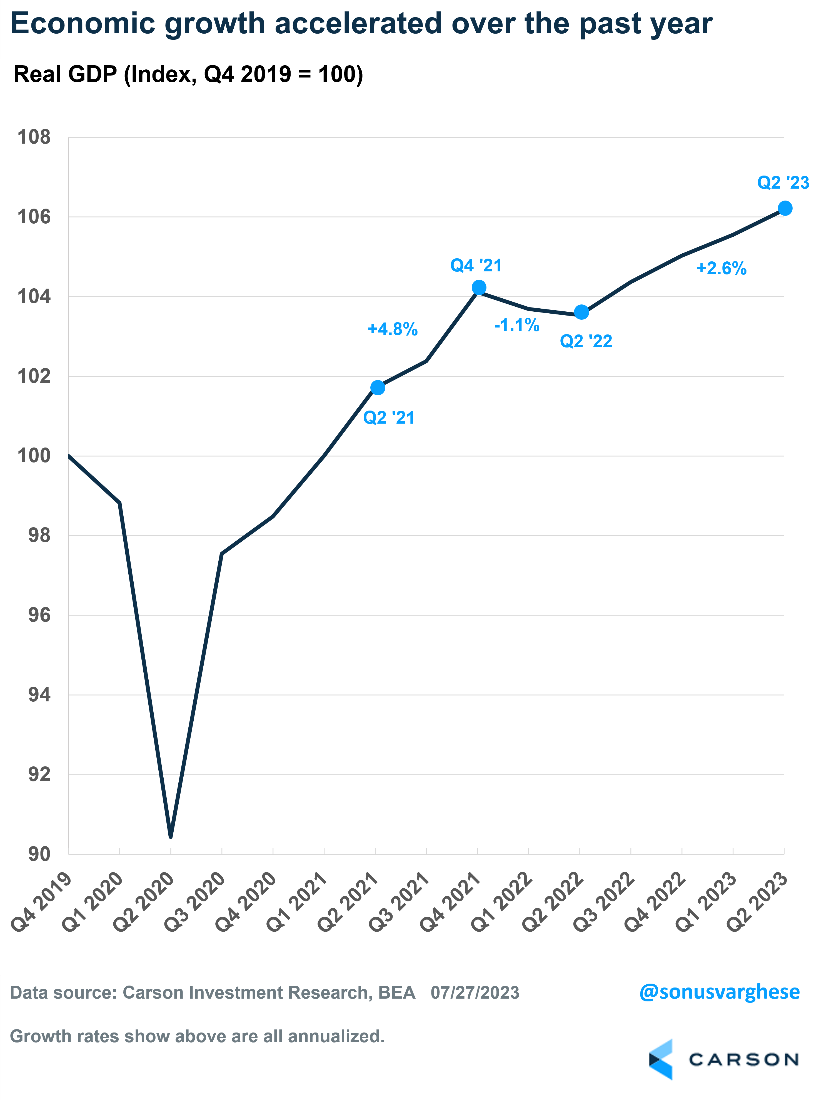

- Economic growth accelerated over the past year, defying tight policy and expectations.

At Carson, we have been overweight stocks all year, expecting strong gains. But we are paying close attention to the fact that some well-known bears have thrown in the white flag and upped their targets. From a contrarian point of view, this could be a near-term warning sign. Another potential concern is August and September are historically two of the weakest months of the year.

To be clear, we do not expect major weakness. But we believe a modest pullback of approximately 5% would be perfectly normal. The S&P 500 has closed higher for five consecutive months, so the odds favor a down month relatively soon. August has been a poor performer, ranking worse than only February and September since 1950, and trailing behind only September and December in the last 10 years.

President Dwight D. Eisenhower said, “Plans are worthless, but planning is everything.”

If the markets experience weakness in the coming months, investors may be surprised. But this would be normal seasonal behavior. It may present buying opportunities, or it may simply be a chance to refrain from panicking and remind ourselves that most years see more than three separate 5% pullbacks per year. Stocks can fall, even they don’t seem likely to now.

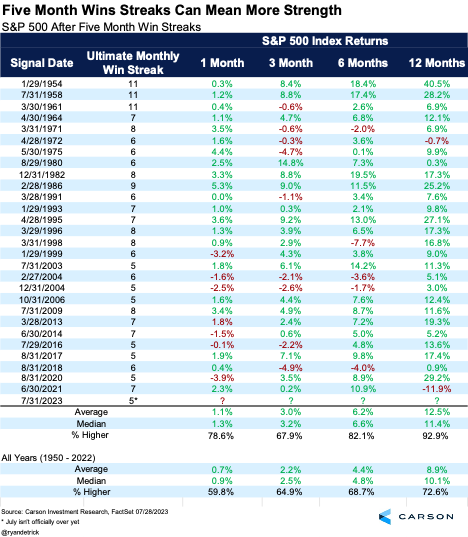

The S&P 500 is set to close higher for its fifth consecutive month today. Historically, stocks have done quite well after similar streaks. In fact, the S&P 500 has been up a year later 26 out of the past 28 times. However, the last time this happened was in 2021, and that was followed by a drop of nearly 12%. Despite this recent example, the market’s strength is likely another indication of higher stock prices in the future.

The Fed Still Believes in a Soft Landing

The Federal Reserve raised the federal funds rates by 0.25% at its July meeting, taking rates to the 5.25-5.0% range — the highest in 22 years.

This was widely expected. In fact, the Fed’s statement behind the decision was mostly unchanged relative to June, except for a subtle but important distinction. Instead of saying the economy grew at a “modest” pace, Fed members said it’s growing at a “moderate” pace.

“Moderate” is Fedspeak for a strong economy. In fact, Fed staff are no longer forecasting a recession, which is a significant shift from the last few meetings.

Simply put, this wasn’t supposed to happen. Last year, when inflation hit 9%, Fed members, along with many other economists and market-watchers, were convinced that they would have to raise rates aggressively, reverse labor market gains, and send the economy into a recession.

They did raise rates — 11 times over the past 17 months. It has been the most aggressive rate-hike cycle in 40 years. But the rest of the story didn’t pan out as expected:

- The economy created 5.2 million jobs since the Fed started raising rates and 1.7 million jobs just over the first six months of this year.

- The unemployment rate was unchanged at 3.6% between March 2022 and June 2023.

- The economy grew 2.4% in the second quarter and has expanded 2.6% over the past four quarters, which is faster than the pre-pandemic growth rate.

- Headline inflation has pulled back from 9% to 3%.

In summary, there was no recession, despite an aggressive Fed. At the beginning of the year, we discussed in our 2023 outlook why this was the likely scenario. Events have unfolded as expected, and if anything, the economic environment looks even better now. (We wrote about this in our Mid-Year Outlook.)

In his post-meeting press conference, Fed Chair Jerome Powell acknowledged that inflation has moderated even as the economy remained resilient. More importantly, he said that is likely to continue.

Core inflation, excluding food and energy, remains elevated, although it has seen a downshift recently. But the Fed is now singing a slightly different tune from last year. They’re saying that inflation can move lower without a significant breakdown in the labor market and a recession.

That means the Fed needs to see core inflation pull lower to end this rate-hike cycle, as opposed to requiring the unemployment rate to climb.

And there’s good reason to believe that core inflation may fall.

Core Inflation Could Surprise to the Downside

Core inflation, as measured by the Fed’s preferred personal consumption expenditures (PCE) index, has run at a 3.4% annual pace over the past three months. The good news is a couple of large categories could send core inflation close to the Fed’s target of 2% over the next year.

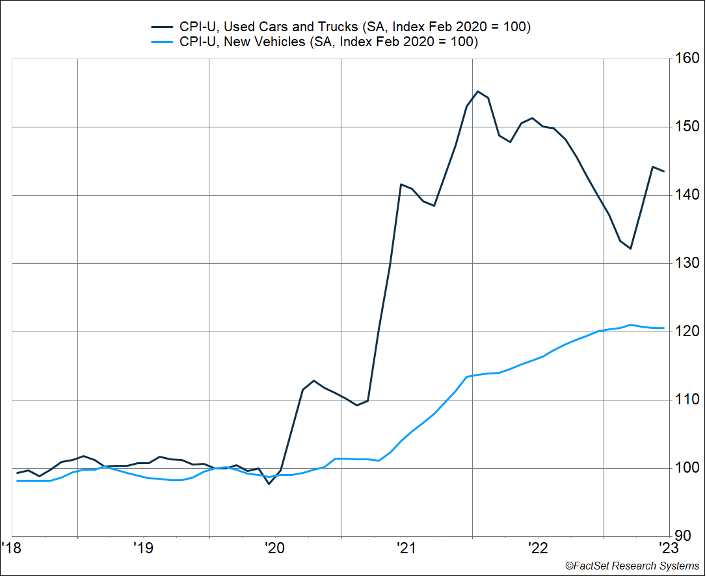

The first is used and new vehicle inflation, which is likely to fall even more than it already has. Wholesale auction prices suggest that used car prices are falling quite significantly, and improved vehicle production should continue to ease new vehicle prices. There’s a good chance that prices fall, i.e., outright deflation occurs, for a category that makes up 10% of core PCE inflation.

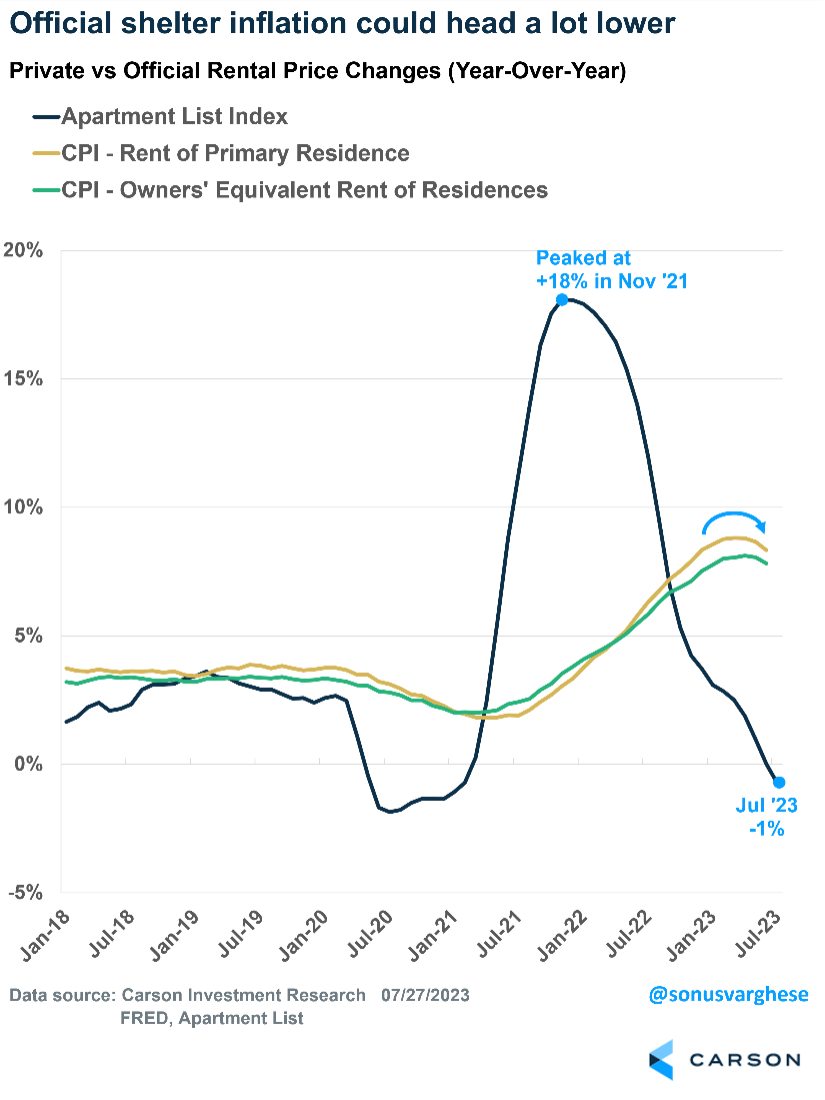

The second is housing inflation, which makes up 40% of core CPI and 20% of core PCE inflation. Housing inflation is currently running at a 5-6% annualized pace. That is down from 8-10% earlier this year, but it is still above the ~ 3-4% pre-pandemic rate.

However, private rental data indicate more deceleration is coming. In fact, the Apartment List data for July indicates rental prices fell 0.7% year-over-year. Additionally, multi-family construction is at a record high, which means more rental units will come online later this year and into 2024, putting more downward pressure on rents.

So, housing inflation may move even lower than it was before the pandemic, perhaps close to 2%. That could easily pull core inflation close to the Fed’s target of 2%, if not below.

This is why we believe there is a high probability of inflation surprising to the downside over the next few months and into next year. If that is the case, the July rate hike was likely the last one of this cycle.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01851028_073123_C