So far, 2022 is faring to have one of the worst ever starts for stock returns. Only 1932 and 1939 have proven to be more difficult through the first four calendar months. The reasons are numerous and front-of-mind for us all: an unexpected war in Ukraine, the lingering impacts of COVID-19, the highest inflation rates in 40 years, and the prospects for a contentious mid-term election right around the corner.

Given all that uncertainty, equity prices in 2022 have seen greater levels of volatility and have dropped into correction territory for the first time since the initial onset of the pandemic in early 2020.

But, this rising collection of market uncertainty comes in stark contrast to the continued relative strength of the U.S. economy, which remains buoyed by strong consumer spending, the healthiest job market in decades, and increased confidence for companies to invest in their business. So why is there such a difference between the good news around the U.S. economy and the pessimistic bearishness of the stock market?

The aggregate behavior of the market – which is essentially the collective of millions and millions of investors – is not simple to assess. But the market’s DNA favors certain reactions to events that happen to unfold. It doesn’t wait for things to become definitively good or bad. Rather it focuses on the possibility of events making the future trend lean better or worse.

That’s why, despite an economy that is continuing to produce favorable outcomes, the market is focusing on uncertain events like rising geopolitical tensions or higher inflation as these trends appear worse than they were last year. For the market, uncertainty means worse. And worse means lower stock prices.

At Carson Partners, we believe that while risks certainly exist, the likely cause for most of this uncertainty is a result of inflection points that the market is having to assess. These inflection points are raising the blood pressure of the market, but we believe they will work themselves out over the near-term. As a result, we remain cautiously optimistic on the prospects for continued strength in the U.S. economy and a likely recovery in stock prices over the second half of 2022.

So what are these inflection points and how might they unfold going forward?

Inflection Point 1: COVID-19 Shifts From a Pandemic to an Endemic

COVID has had an incalculable amount of destruction on this world. The loss of life. The economic impact on businesses. The cancelled opportunities and memories with friends and families. It’s been a tough two years.

But what we are likely going through right now is the inflection point of COVID going from a pandemic (widespread, simultaneous uncontrolled infectious disease) to an endemic, where the virus may remain a significant health threat but it becomes more seasonal and predictable similar to other communicable diseases. And while this inflection point of a pandemic unfolds, right now we are living through the by-products that affect way more than just our health.

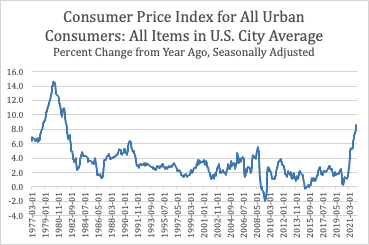

The reopening of the world post-pandemic is one of the major reasons that inflation is surging. The combination of businesses trying to get back up to speed after being shuttered through the pandemic (picture a car that hasn’t started in a year trying to get going again), mixed with the pent-up demand of Americans ready to upgrade the house they’ve been confined to, go on a vacation, or get a new car, is creating an inbalance of supply and demand that is putting pressure on prices of everything from eggs to airfare to housing. And the result is the highest inflation rates in four decades.

Chart 1: Inflation at Multi-Decade High

Source: Bureau of Labor Statistics, Carson calculations

So many are focused on the level of inflation – understandable given the impact on our wallets – but it’s the reasons for it that often take a back seat. And while inflation is influenced by many facets, the primary elements stem from the by-product of living through a pandemic. For example, the trillions and trillions in fiscal stimulus (pandemic relief) was necessary to help struggling Americans. But its impact is felt in inflation today as so many used the extra relief to purchase (even hoard) goods, which drove prices higher.

Another example is the restarting and reopening of America post-pandemic that has so many feeling a sense of pent-up demand for services. This is showing up as delayed elective medical procedures that are now lined-up as far as the eye can see. It’s proper haircuts, the Friday nights at the favorite eatery, and that much needed vacation. And with it, more people are out and about, demanding services to an already fragile economy just gearing up from its pandemic hiatus.

But so much of this inflationary pressure appears to be transitory – the mix of pent-up demand and a business environment still reopening. Inflation doesn’t just happen. In this instance we are living through today, the root cause is the downstream and inflection point impacts of COVID.

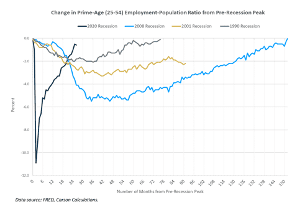

But this pandemic-to-endemic inflection point is showing up in our economy and lives in far more examples than just inflation. It has also changed the labor force and the way talent works forever. The shift to more virtual, work-from-anywhere employment is here to stay. The good news is that this flexibility did more than just make work easier for many Americans. It also allowed businesses to rehire at the fastest rate coming out of a recession in recent memory.

Over the three prior recessions, it took at least six years for the employment-to-population ratio to revert back to pre-recession peaks. But this recovery is so much faster as it has almost fully recovered in just two years. This is good news for families as it means faster rehiring and less lingering unemployment. But it also means faster spending of paychecks, which results in more purchases before businesses can even ramp up supply chains to meet the demand. The result? Higher inflation.

Chart 2: Labor Markets Have Healed From COVID

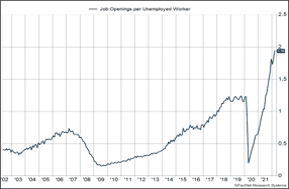

In fact, to just keep up, businesses are opening new jobs at the fastest rate ever recorded. The result is 1.94 open jobs for every unemployed person – by far the most ever. Again, that is great for the worker who has more opportunities. But it also means that businesses are competing for employees, which drives wages up and results in inflation.

Again, this doesn’t just materialize out of thin air, it’s the result of the inflection point from pandemic to endemic.

Chart 3: Open Jobs Are Outnumbering Unemployed Workers

Source: Bureau of Labor Statistics, Carson calculations

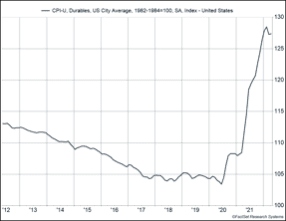

The good news is that as this inflection point works its way through, the inflationary pressures will begin to subside. And there are signs that this is beginning to happen. In areas like durable goods – things like washing machines and lawnmowers – inflation appears to be rolling over. Americans who spent so much time in a pandemic-lockdown upgraded home items. This resulted in inflationary pressures. But that cycle is likely to have peaked.

Chart 4: Goods Inflation Appears to Be Peaking

Source: Bureau of Labor Statistics, Carson calculations

Inflection Point 2: Policies Shift From a Tailwind to a Headwind

Another inflection point is the shift from accommodating aid from governments and agencies to a new environment of hawkish and tightening policy. In other words, the spiked punch at the economic recovery party is being replaced with black coffee. Fiscal spending, which was trillions in aid, has come to an end. And now, monetary policy from the Federal Reserve is in its inflection point from the tailwind of near-zero interest rates to the perceived headwinds of tighter financial conditions.

Chart 5: The Fed’s Path to More a Normalized Rate Environment

Source: Federal Reserve, Carson calculations

The Fed has already raised rates two times this cycle and even elected for the rare 50-basis-point increase for the first time since May 2000. Rates have been near zero since 2008, outside of a quick rate rise in 2017–19.

It is not normal, nor even healthy, for a zero-interest rate policy in perpetuity for many reasons. A primary reason is that while rising rates will increase interest paid on debt, Americans in aggregate actually receive twice as much interest income as they paid out. As a result, rising interest rates to normal and healthy levels actually benefits the average American twice as much as it hurts them. For evidence, just look at that paltry level of interest you’re receiving from your bonds and your savings account.

But once again, it’s this shift in the inflection point of accommodating to more restrictive policies that has the market feeling uncertain. But as this uncertainty wanes through the playing out of this shift, markets should express their comfortability through lower volatility.

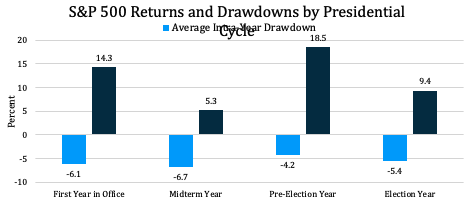

Inflection Point 3: The Four-Year Presidential Cycle Hits its Mid-Point

The endless swarm of political ads are coming. So is the rhetoric from both sides of the aisle that things are bad and need changing. This brings more than just ramped-up political tensions. This inflection point serves as a level of uncertainty for markets regarding the future path of policy and the make-up of decision-makers. As a result, the second of the four-year presidential cycle is usually the most volatile leading up to the mid-term elections.

Chart 6: The Mid-Term Year Is the Most Challenging of the Presidential Cycle

Data Source: Morningstar Direct, Carson calculations. Calculated using S&P 500 TR Index monthly returns from 2.1.1970 to 4.30.2022. Data are also adjusted for Nixon and Ford’s partial term.

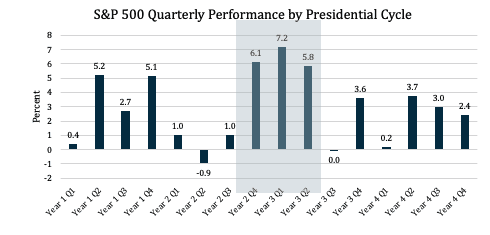

Going back to 1970, the second year of the presidential cycle has been by far the least rewarding for equity investors – averaging 5.3%, which is nearly half or less than the other three years. In addition, the average intra-year pullback is higher, reflecting the increased level of uncertainty and volatility for the market. The good news, however, is that history shows the very best periods of equity returns have usually occurred after this mid-term election inflection point. In fact, starting with the fourth quarter of this year, the best three quarters on average of the four-year presidential cycle since 1970 have materialized as the inflection point of uncertainty dissipates.

Chart 7: Post Mid-Terms Have Been a Strong Seasonal Benefit to Stocks

Data Source: Morningstar Direct, Carson calculations. Calculated using S&P 500 TR Index monthly returns from 2.1.1970 to 4.30.2022. Data are also adjusted for Nixon and Ford’s partial term.

Conclusion

It’s important to note that market volatility is both commonplace and healthy, especially after the greater-than-100% rally in stocks following the pandemic lows just over two years ago. In fact, since 1980 every single year has seen a pullback in stock prices, with the average being around a 14% decline. And while market dislocations are never a pleasant experience, they have rewarded patient, long-term investors with attractive entry points. Of the 33 market corrections since 1980, 90% of them saw gains over the following year – averaging ~25%.

Our view remains that we are near or even past the peak of inflation and with a limited but swift series of interest rate hikes, the Fed can curb inflation further while creating a soft landing for the economy. Furthermore, the market is unsettled, having to deal with three or more simultaneous inflection points that are driving uncertainty and volatility. But as these shifts unfold through the rest of 2022, we expect equity markets to stabilize and reverse course.

We continue to stress that the best course of action is patience and sticking to your investment plan, which has incorporated anticipation of volatility like we’re facing today. If history has proved anything it’s that the market, like most things in life, is more fragile than we might expect in the face of uncertainty over the short run. But it’s far more resilient over the long run than we often give it credit for.

Evidence of this stands right before us given the realization of just how far we have come since the pandemic’s onslaught two years ago. Then, it was the inundation of cancellations – everything from shuttered workplaces to closed schools, cancelled graduations and public gatherings. But our optimism for the near-term future was never cancelled. Neither was our hope. The long-term prosperity of America remains, as do the attractive prospects for long-term investors that patiently benefitted from the market’s recovery and our nation’s healing.

Our future was never cancelled, and it certainly isn’t today. It has just ignited our resolve.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.